Their economic development has occurred in parallel to the development of the insurance industry, which plays an important role in supporting the health systems of these nations, coping with natural disasters and climate change risks, protecting the assets of the budding middle class, and sustaining the progress of many companies, among other activities where it has a significant presence.

On the negative side, emerging countries face significant risk exposures and annual losses that remain uninsured, even though the capacity for much broader insurance coverage is there. Although protection gaps exist all over the world, they are greatest in emerging and developing nations, where their consequences are most damaging because of the lack of state resources to address losses.

The Geneva Association, the leading international insurance industry group, recently published a report taking stock of the growth experienced and outlining the challenges ahead, many of which are linked to public-private partnerships.

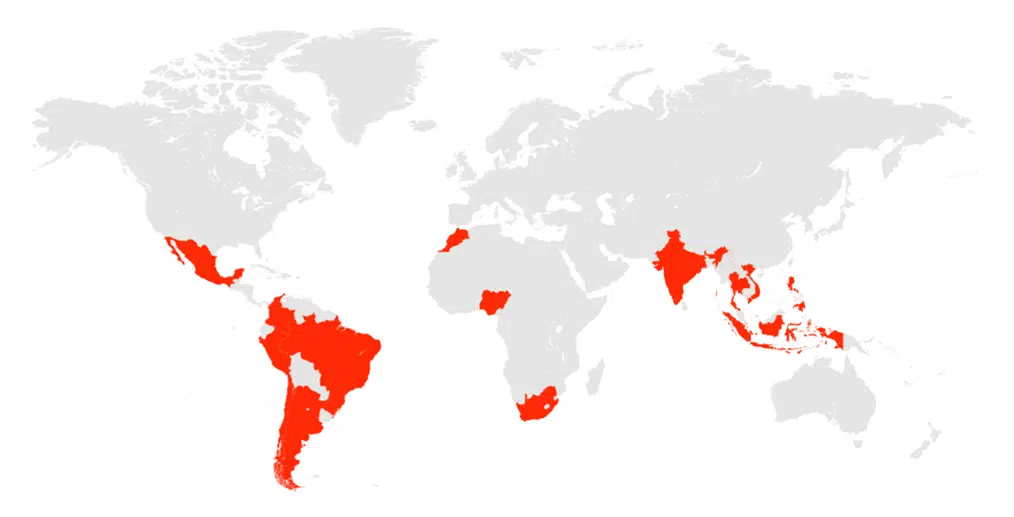

The study focuses on fourteen countries in Latin America (Mexico, Colombia, Brazil, Peru, Chile, and Argentina), Africa (Morocco, Nigeria, and South Africa), and Asia (India and four Southeast Asian nations: Thailand, Vietnam, Indonesia, and the Philippines). Together, these countries have a combined population of some 2.8 billion people and a market which had 332 billion dollars in insurance revenue by the closing of 2020, more than the GDP of several of the countries on the list. For its part, Mapfre has millions of customers in the emerging world, mainly in Latin America, where it is the largest insurance company.

Economic development and insurance level are often linked

In these countries, from 2005 to 2020, insurance penetration (the percentage of the country’s economy as a whole that is represented by the insurance business) has risen from 1.9% to 3.3% on average. While highly significant, this progress is still miles away from the most developed economies. In the OECD (which includes a large part of Europe, the USA, Canada, and other high-income countries such as Israel and Japan), the share of insurance in GDP was 8.6% in 2005; by 2020, it had already reached 9.4%.

Generally speaking, economically stronger countries have higher levels of insurance. For their part, and although they have markedly different characteristics, emerging countries face a series of common issues. Among others, the Geneva Association points to the legal framework in these countries, whose rigidity often acts as an obstacle. Consider the fact that some countries require a paper copy of any policy, a reality which severely limits the possibilities for microinsurance where digital solutions are crucial.

Offering basic risk coverages targeted at low-income populations, microinsurance policies are particularly relevant in emerging nations. Nevertheless, millions of people are unaware that they can access these protections at affordable prices. This ties in with another major problem: a lack of financial education.

Beyond income levels, there are cultural aspects that explain the low penetration of insurance in Latin America, Asia, and Africa. In many countries, the general population relies on informal protection mechanisms. For example, if a member of a community becomes ill, it will be his or her own relatives who come to their aid. While these mechanisms may work on an individual basis, they cannot respond to risks that endanger an entire community, such as a bad harvest, a pandemic, or a natural disaster. In this respect, recent events such as COVID-19 or the climate change debate have brought awareness to risk and the role of insurance, as the report highlights.

Public-private partnerships, an essential ingredient for financial inclusion

The Geneva Association calls for greater public-private collaboration, including financial literacy and education, regulations that spur innovation and development, and policies that encourage access to insurance, of which there are many success stories. India launched a program in 2015 to enable people without access to a standard bank account to set up a free account with a network of partner banks. Additionally, the account provides basic accident insurance free of charge. Since its implementation, around 50% of the country’s rural population—more than 400 million people—have benefited from this scheme, rendering it a good example of how governments, banks, and insurance companies can cooperate to promote financial inclusion, claims the study.

Carlos Rami, Group Head of European & International Affairs at Mapfre, who helped prepare the report, details the importance of this public-private partnership: “Public policy and regulation play a key role in the development of sound markets. To favor a solid and competitive insurance market is to favor economic and social progress, and it cultivates an environment where individuals comply with their commitments, even when risks materialize.”

“That is why we believe it is vitally important to promote public-private collaboration frameworks that allow insurance to act where society needs it most, both in the coverage and risk management that may affect a given jurisdiction and in promoting financial education in society and product innovation,” says Carlos Rami. Looking ahead, he believes that “while emerging countries represent a promising market for top-tier insurance groups such as Mapfre, it is necessary to continue to identify the barriers and obstacles affecting insurance operations and work with regulators to remove them. In this respect, regulators are key to the development of strong compliance guarantees, such as the insurance industry, in the societies and countries under their jurisdiction.