ECONOMY| 23.02.2022

How to start saving and investing

Some months it’s easier, others it’s harder, and there are months when it’s best to not even think about it, but saving money is a goal for just about everyone. You may have already taken the first step and built up some savings, or you might just be considering it. But once you’ve done the hard part, we have some tips to help you get the most out of your money.

You’ll need to consider circumstantial factors like the inflation rate, an old acquaintance for economies in Latin America that is making a powerful comeback in Europe and the United States. There are also more general and even personal aspects to keep in mind, such as risk, terms, and knowing what type of investor you are, or the mistakes that newbie investors tend to make. So, with the help of the team at MAPFRE Gestión Patrimonial (MGP), let’s have a look at all the variables you need to consider in order to start saving and growing your money.

Inflation

Several factors have caused inflation worldwide to soar to its highest level in decades. Ismael García Puente, investment manager at MGP, attributes this situation to government spending to handle the pandemic, the huge amounts of money created by central banks, the problems affecting supply chains and global transport, and rising energy costs amid the ecological transition.

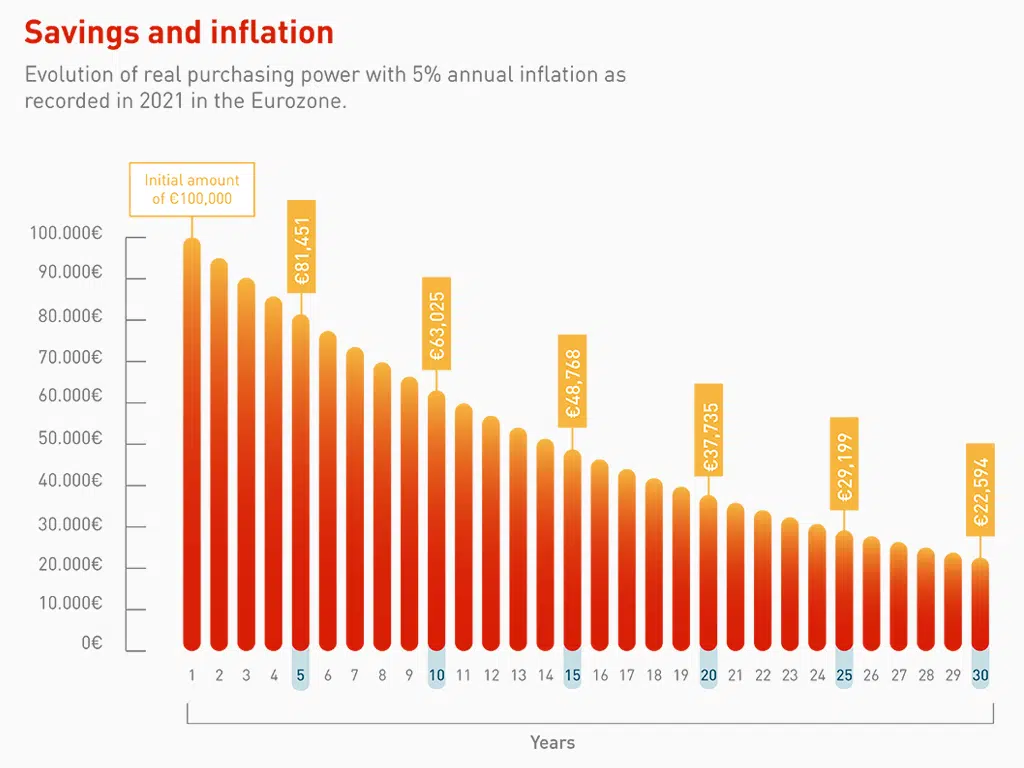

As prices climb, your savings lose purchasing power, a slow yet inexorable process clearly represented in the chart below. In 2021, the inflation rate in the Eurozone stood at 5%, according to Eurostat. Using this figure as a reference, we can simulate real purchasing power over time: as you can see, it starts to decline rapidly, and after 15 years it’s less than half of what it was at the outset.

Having your money tied up in a CD, which is still one of the most common forms of savings, is not the best option. Beyond a certain amount you should always have on hand for common expenses, once you manage to save, it’s a good time to start combining your savings with investing. And at this point, we need to talk about real returns: in an environment of 5% inflation like the one in the example, you have to subtract that amount from your earnings from any product; if it’s lower, your investment is costing you money.

Types of investors

To find the best strategy, you need to know what type of investor you are. And this has more to do with your time horizon than your risk tolerance, although both concepts come into play. MAPFRE Gestión Patrimonial distinguishes between the following four risk profiles:

- Conservative

A conservative investor is looking to cash in on their savings within at least a year and a half. Therefore, they will mainly invest in fixed income (debt), a more conservative option because there are usually fewer variations in its market price compared to equities (shares), although it also has lower returns. The objective is to always maintain volatility at less than 5% annually.

- Moderate

This type of investor considers a time horizon of more than four years, so they can look for a balance between fixed income and equities. Fluctuations in capital would be somewhat higher, up to 10% per year.

- Aggressive

Here, the term increases to more than six years, and investments have a higher percentage of equities. These investors can also expand into other markets, such as Europe, the US, Asia… The price fluctuations will be greater, with the aim of keeping them at less than 15% per year.

- Very aggressive

An investor with higher risk tolerance sets a goal of eight years or more. That way, they can look for the best opportunities in equities worldwide. In this profile, there is no volatility control.

Long-term strategy

As you can see, risk tolerance is closely linked to term. The longer your time horizon, the better your chances of getting a good return on your savings, and the less risk you will be exposed to. This is fundamental for anyone who wants to learn how to invest: you have to think long term.

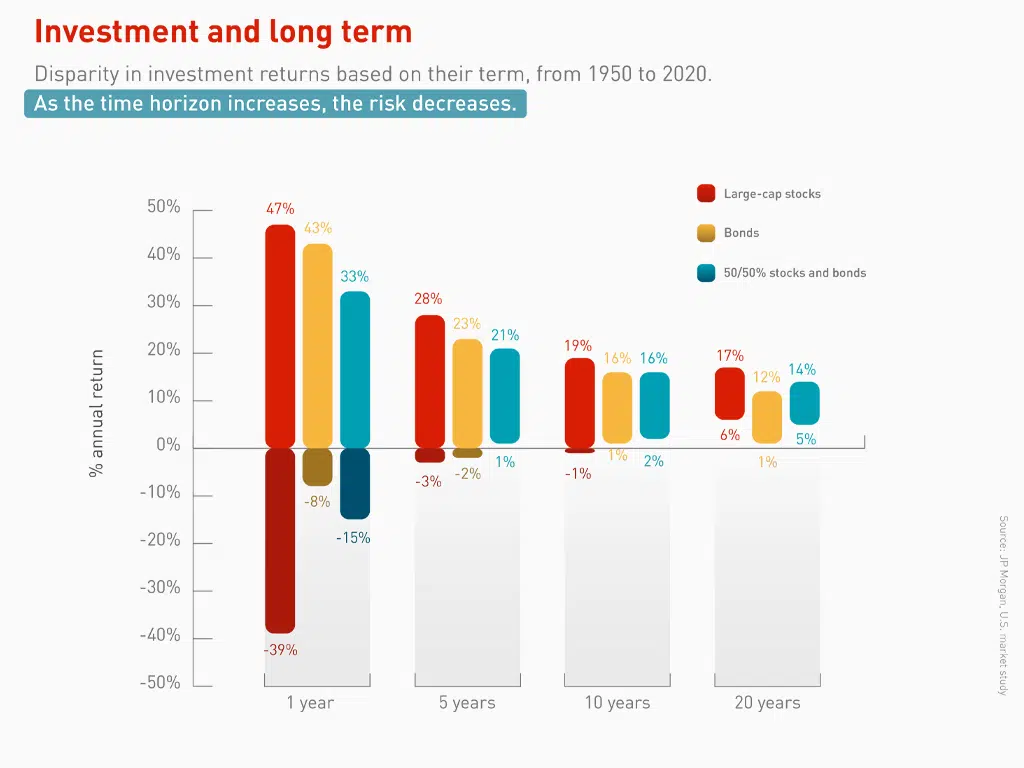

The image below shows the historical evolution of various types of investments: shares in large companies, debt bonds, and a portfolio of 50% of both, in this case, in the US market. The percentages are the maximum and minimum annual returns for various periods, which is known as the dispersion of return. Notice how, as the investment term lengthens, the risk decreases, and anyone who had invested for 20 years since 1950 would have grown their savings.

“By understanding risk and having a long-term vision, we can reduce it as much as possible. In this case, we can see that the probability of loss over 20 years is negligible, there would be hardly any risk,” explains Daniel Sancho, head of Investments at MGP.

Diversification

To minimize risk, spreading your assets over several sectors and even geographical areas is a good investment strategy. By not putting all your eggs in one basket, the potential losses of some of your investments can be offset by the rest.

In fact, what many people consider to be a cautious investment may not be one at all. Let’s look at the example of a real-estate investment: buying a home as a rental property. If we were to ask our readers if they consider it a cautious option, many would say yes. However:

- All of your equity is in one asset, in a single sector and in a certain place, where the conditions may change. All of this is subject to huge variations in price.

- A conservative investment profile is less than two years. When buying a home, you need to consider a much longer term.

- It has no liquidity. With other options, you could cash out right away, whether you need the money or its price is going down. With a home, you would need several months minimum.

- In many cases, it’s necessary to borrow money up front.

- There are fixed and unexpected costs: taxes, condominium fees, repairs, and even the time you spend looking for tenants.

With all of this in mind, buying a home might not be the best option. Thanks to globalization and the development of financial markets, today it is possible to invest globally, in a diversified manner, in a simple and affordable way, using instruments such as mutual funds.

Regular savings

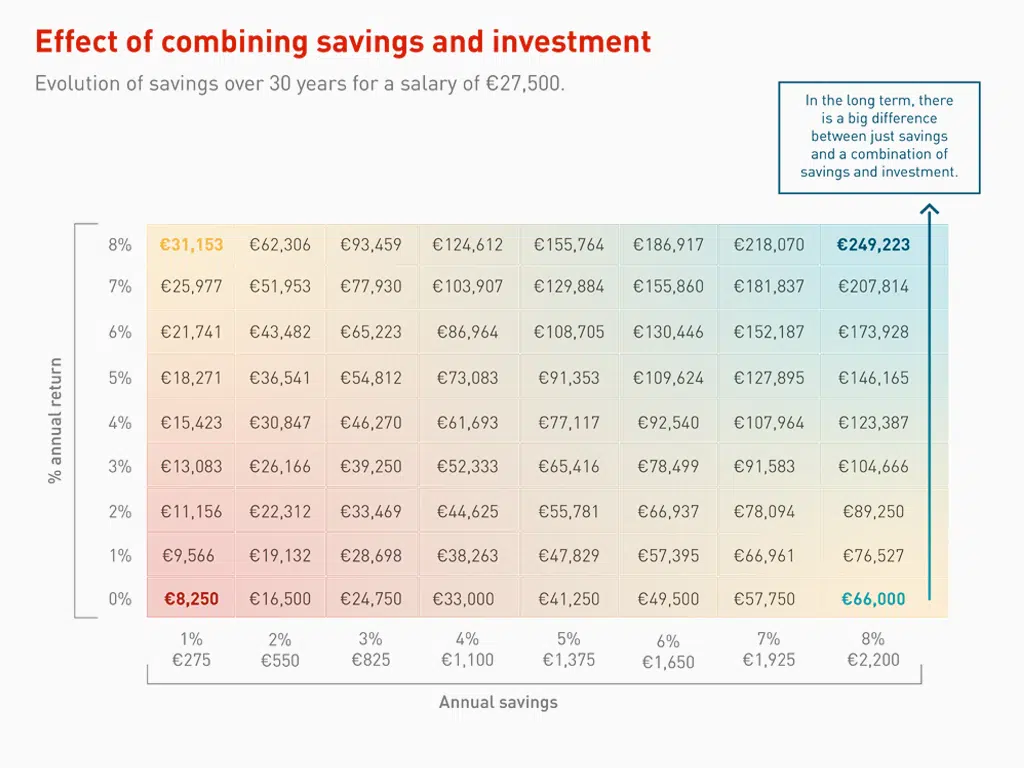

If you manage to contribute regularly to your investments, over time you will see excellent results. This is also the best way to forget about the short-term performance of the markets. This table shows a simulation of the savings growth of a person with a salary of 27,500 euros, according to the amount they save each year and the annual returns obtained.

As you can see, the combination of saving and investing can lead to surprising results.

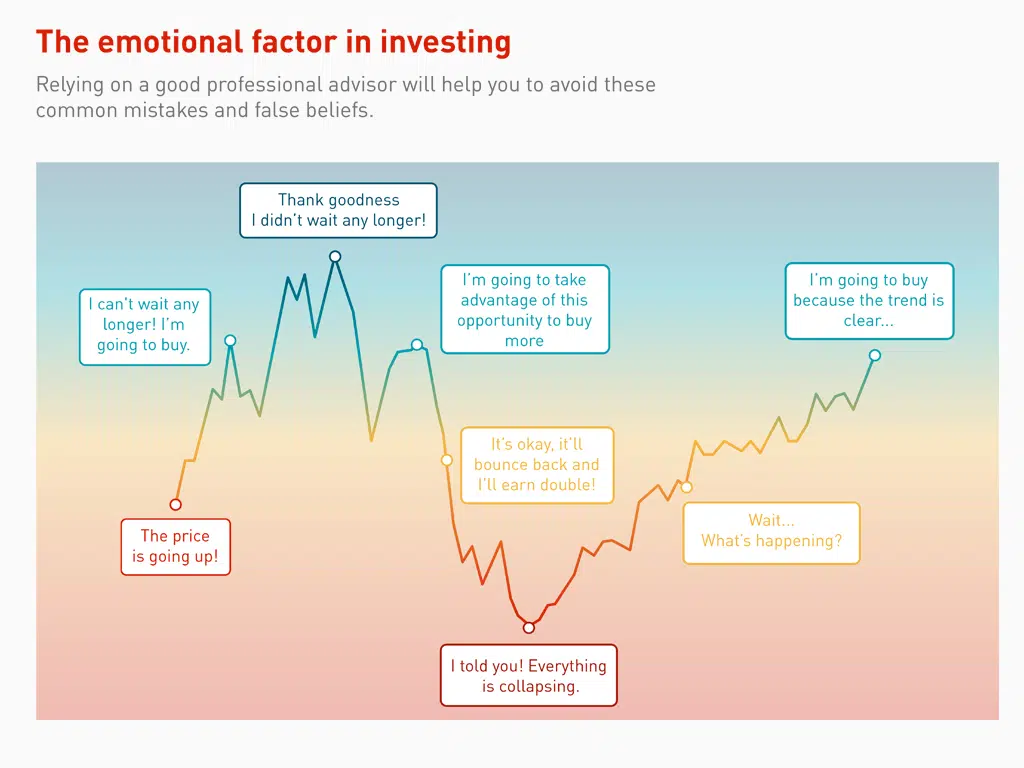

Trust the professionals

The value of your investments will go up and down, along with the fluctuations in the market. They can behave unpredictably, especially for someone who is unfamiliar with the market. That’s why it’s best to have a long-term strategy, as we have seen. And another smart decision is to seek help from professionals, who will know how to identify opportunities and give you the best advice. A good advisor can help you avoid common mistakes like the ones in the chart below.