Mapfre Economics, which is Mapfre’s economic research service, has updated its Global Insurance Potential Index (Mapfre GIP) using the latest available data for the year 2022. This benchmark is based on a series of indicators and metrics that assess the ability of insurance markets to create and consume the so-called Insurance Protection Gap (IPG), in other words, the difference between protection needs and actual existing coverage.

According to this report, in 2022, the global insurance gap came to a figure of USD 7.8 trillion, 14.3% up on the previous year, equivalent to 7.8% of global GDP. The Life insurance segment accounts for 69.1% of this figure and the Non-Life segment for the remaining 30.9%. What’s more, more than 77.6% of the current insurance gap is in emerging markets, a reflection of their great potential for growth.

“Last year, the total IPG was expected to grow at a slower rate than in 2021, on account of factors including inflation and geopolitical uncertainty. In 2022, this has indeed been the case (16.6% in 2021 compared to 14.3% growth in 2022). These forecasts are harsher for the coming year, as the transfer of price increases to insurance policies takes time and, therefore, the penetration rate should, in the best of cases, remain at similar values,” explained Manuel Aguilera, general manager of Mapfre Economics.

However, the GIP not only reflects the current status, as Mapfre Economic Research analyzes its performance ever since 1990. Specifically, when observing the dynamics of the insurance gap since then, several important conclusions can be made. The first is that the insurance gap in the Life segment has grown faster than the Non-Life segment. In turn, when it comes to the Life insurance segment, BRICS nations and other emerging countries have grown the most between 1990 and 2022. And the third is that the G7 and other developed countries, which account for a greater volume of premiums, have experienced more modest growth in this indicator; However, they are the only ones to have grown over the 32 years since records began.

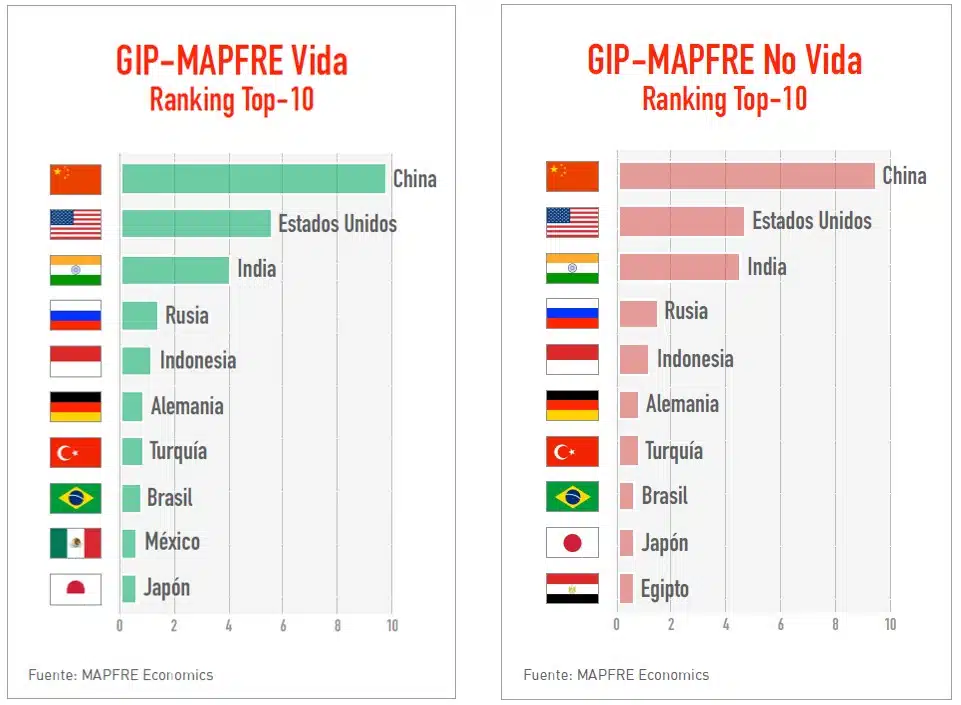

The Mapfre GIP is calculated for 96 insurance markets, for both developed and emerging countries. In its estimation, in addition to the IPG, other variables including but not limited to insurance penetration (premiums/GDP), the size of the economy and the population are taken into consideration. The index generates a score that ranks each market based on its ability to close the global insurance gap, meaning that currently, China, the United States and India are once again leading the ranking of the countries with the greatest insurance potential in both the life and non-life segments.

The report also places an emphasis on the category of “promising markets,” which are countries with major potential to close their insurance gap, but that at present do not have sufficiently relevant economic influence. This positions them lower in the ranking, although they represent an important source of insurance potential moving forward. If these promising markets increase in economic size over time, they could overtake other emerging markets in the long-term insurance potential index.

You can read the full report here