Sara is fully vaccinated. Her family is healthy. She’s been lucky enough to have kept working all the way through the pandemic. As 2021 comes to an end, Sara is feeling cautiously optimistic about both rising vaccination levels and the economic recovery. She hasn’t made any large purchases over the last 18 months and decides that now is the time to change her car. Sara works in the city center and uses public transport to get to work. At the weekends she likes to get out of the city and explore the countryside with her friends and her beloved dog, Charlie. After doing her research online and chatting in a few auto forums, Sara decides to buy a hybrid SUV. She goes to a dealer, takes the car for a test drive, configures the model she wants and negotiates the price. But when the sales representative tells her that she will have to wait at least four months to take delivery of her new car, Sara is amazed. How can it possibly take so long?

Welcome to the reality of the global supply chain crisis

First off, let’s be clear on what a global supply chain is. According to the Chartered Institute of Procurement and Supply, it’s a “network that spans multiple continents and countries for the purpose of sourcing and supplying goods and services.” As the saying goes, a chain is only as strong as its weakest link. In today’s globalized world, all manufacturing companies rely on their supply chain networks to have the components they need to assemble their products when they need them, in the location they need them, and at the time they need them. This just-in-time (JIT) system of outsourcing gives manufacturers a lot of flexibility and allows them to concentrate on those aspects of their offering where they can add the most value. For example, the average family-sized car can contain up to 30,000 individual parts. It makes absolutely no sense for a car manufacturer to have huge factories all over the world, each one producing all the parts they need to assemble the different cars in the company’s product range. It is much more efficient to have thousands of expert and qualified suppliers make these parts and ship them to hub locations where the cars can be assembled quickly.

But serious problems can arise when one of the links in the chain breaks. And if many links in the chain break, global production lines can grind to a half very quickly. And the consequences of that supply chain rupture lasting longer than anticipated may be significant for the economy. “Growth expectations are being lowered due to supply chain tensions. Transportation bottlenecks are the greatest stress point, but limited excess domestic production capacity, low inventories, the steep rise in input costs (most acute in the case of raw materials), and labor market challenges are all making it increasingly difficult for supply to keep up with demand,” states the latest Mapfre Economics Panorama report.

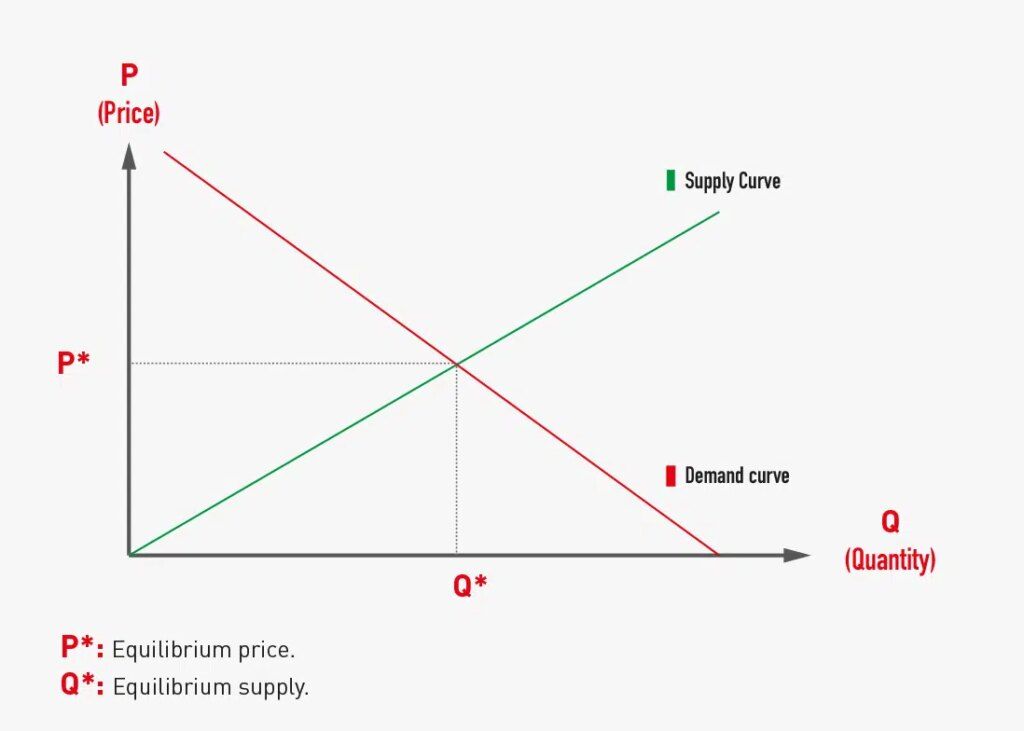

So now let’s go back to the question of why Sara can’t get new car for four months, (or maybe more). The answer lies in how one of the most fundamental aspects of modern economies works: the law of supply and demand. Demand is all about what you want and how much you are willing to pay for it. The law of demand says that at higher prices, buyers will demand less quantity of a given economic good. Supply is all about market operators getting the products and services you want to your door. The law of supply says that at higher prices, sellers will supply higher quantities of a given economic good. When these two laws interact, as shown in the graph below, they determine the actual market prices and volume of goods that are traded on an open market in normal conditions.

The point of intersection between supply and demand is called price equilibrium – a particular good or service will be delivered to the market (Q*) at a particular price (P*). From that initial point of equilibrium, there are four possible scenarios:

Demand goes up

If demand goes up and supply doesn’t follow it, the result is a shortage of the product or service, meaning the price will go up. (Think about the rise in demand for face masks at the outbreak of the COVID-19 pandemic.)

Demand goes down

If demand goes down and supply doesn’t follow it, the result is a surplus of the product or service, meaning the price will go down. (Think about the sharp drop in demand for children’s toys in January.)

Supply goes up

If supply goes up and demand doesn’t follow it, the result is a surplus of the product or service, meaning the price will go down. (Think about the huge increase in the supply of electric scooters over the last few years.)

Supply goes down

If supply goes down and demand doesn’t follow it, the result is a shortage of the product or service, meaning the price will go up. (Think about the fall in the supply of lorry drivers in the UK recently.)

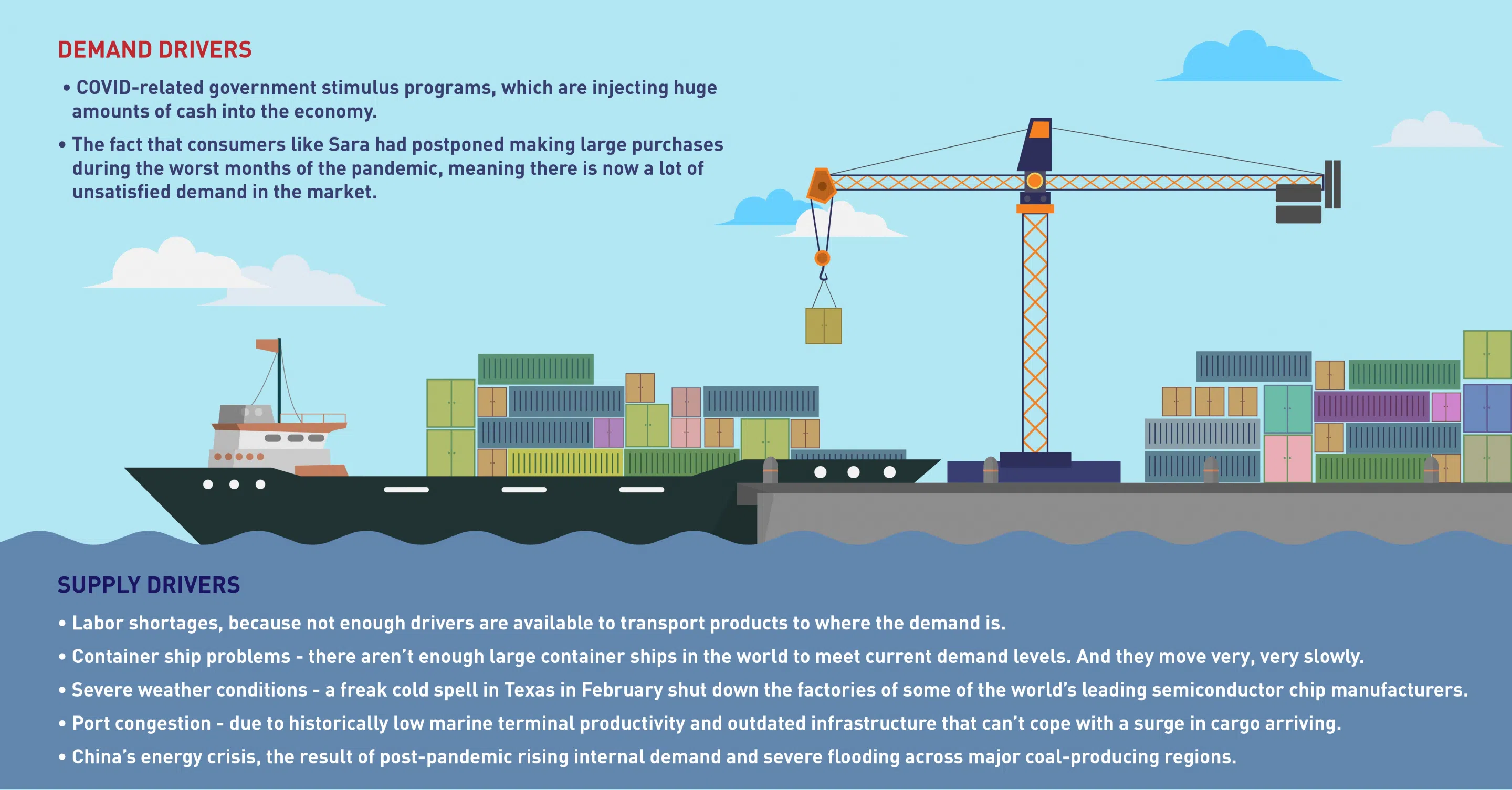

As we said earlier, when supply and demand intersect, the market price is established. When supply and demand shift, the market price fluctuates. Recently, we have seen significant shifts in both supply and demand:

When you put all of these factors into a pot and mix them together, what you get is a situation where demand is structurally higher than supply, which in turn leads to delays, shortages and increased costs across every element of the global supply chain.

All of this impacts on inflation – Sara’s cost of living – which may end up conditioning monetary policy decisions: “The inflationary prospects already perceived by the main central banks still rest on the idea of an upturn of a limited and transitory nature. However, the odds that the scenario will come to fruition are reduced as global supply chains continue to encounter obstacles, bottlenecks accumulate and the shortage of certain goods expands towards the initial productive phases composed of raw materials and energy ”, explains Mapfre’s research department.

And that is why Sara will have to wait four months to collect her new car.