In the developed world, citizens have several safety nets that allow them to mitigate the impact of an unexpected event, such as the one that many of us have been living through in these last few months. The tools provided by industry activities can also be added to the aid, subsidies and other facilities that the public sector makes available to companies and individuals.

In developing countries, these safety nets do not exist in most cases. A person working in the informal economy who is sick or suffers an unexpected shock is exposed to a loss of wealth and income that affects their whole family and can condemn them to a situation of poverty.

That is why it is important to explain the role that insurance can play in financial inclusion, in order for these lower-income groups of society to gain access to the products that enable them to protect their life, health and assets, through the savings and loss compensation processes implicit in insurance products.

In this sense, insurance is a mechanism that can facilitate social mobility by allowing individuals and families to overcome shocks that, over the course of their lives, can affect their wealth and future income-generating capacities. Without the support of insurance, individual or family progress can be lost to certain adverse events. Thus, the possibility of accessing insurance products and services may be the difference between individuals or families achieving the goal of social mobility, or remaining in a situation of economic vulnerability.

This is highlighted by the latest report on financial inclusion in insurance, recently published by Mapfre Economics, which provides a conceptual and international analysis of how microinsurance can contribute to the objective of financial inclusion and to increasing opportunities for a very broad segment of society to have access to higher levels of well-being.

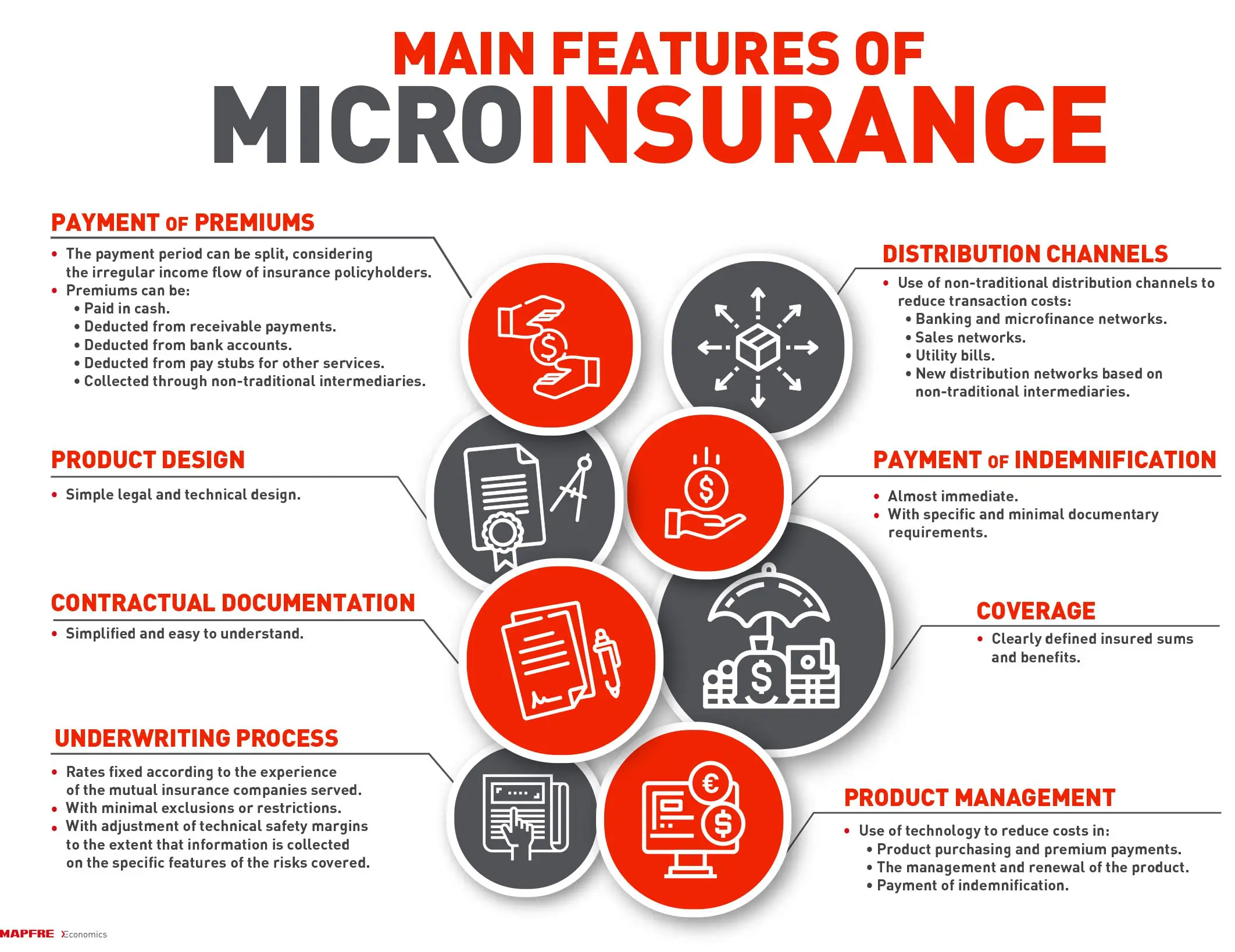

The term “microinsurance” is used to refer to insurance for low-income populations, which may fall within a broader category called “inclusive insurance” — insurance intended for groups generally excluded or under-served by the insurance market.

As explained in the Mapfre Economics document, two factors have been influencing the development of microinsurance in recent years. “The first is the willingness of public authorities to stimulate its growth as part of the design of specifically created public policies; and the second is technology, which can facilitate access to a broad group of potential policyholders (even in rural areas) at a reasonable cost.”

The use of suitable technological platforms is essential to reduce costs not only in purchasing the product and paying the associated premium, but also in its management and renewal, and in the payment of the corresponding indemnification.

The microinsurance product must have a simple design, both from a legal and a technical point of view. From a legal point of view, the policy and its terms and conditions must be simple and its content easy to understand. And from a technical perspective, it must include simple coverage and clearly defined insured sums and benefits.

Microinsurance must be designed in such a way that indemnification payments are made almost immediately, with specific and minimal documentary requirements.

Latin America, well positioned to develop inclusive insurance

Obviously, the development potential of such products is greater in countries that do not have a developed financial industry or sophisticated products. In this sense, Latin America has the optimum conditions for developing inclusive insurance products.

The Economist Intelligence Unit, with the support of the Inter-American Development Bank (IDB), among others, publishes an annual report with indicators to assess the environment for financial inclusion in more than fifty countries. This translates into an index that takes five aspects into account: governance and policy support; stability and integrity; products and points of sale; consumer protection; and infrastructure.

The 2019 report concludes that the global environment for financial inclusion is improving, with Latin America being the leading region for financial inclusion in terms of infrastructure and regulation. Thus, among the first five countries of its ranking, four are Latin American countries (Colombia is number one, followed by Peru, Uruguay and Mexico). India comes in at fifth.

Life insurance, the most common microinsurance

Temporary term Life insurance is currently dominant in the microinsurance market. This is a temporary insurance policy in the event of the death of the insured, in order to protect their family. This policy is often combined with additional accidental death or disability coverage and/or funeral expense coverage, both for the policyholder and the family members designated by the policyholder.

In short, as the authors of the report explain, “inclusive insurance is one of the main tools for bridging the Insurance Protection Gap (IPG) in emerging economies, as it acts in two ways. In the short-term, it raises demand for insurance by bringing new segments of the population within the system of protection provided by insurance. In addition, inclusive insurance is also a means of financial education that will support the social and economic development of the population and ultimately increase the demand for insurance.”