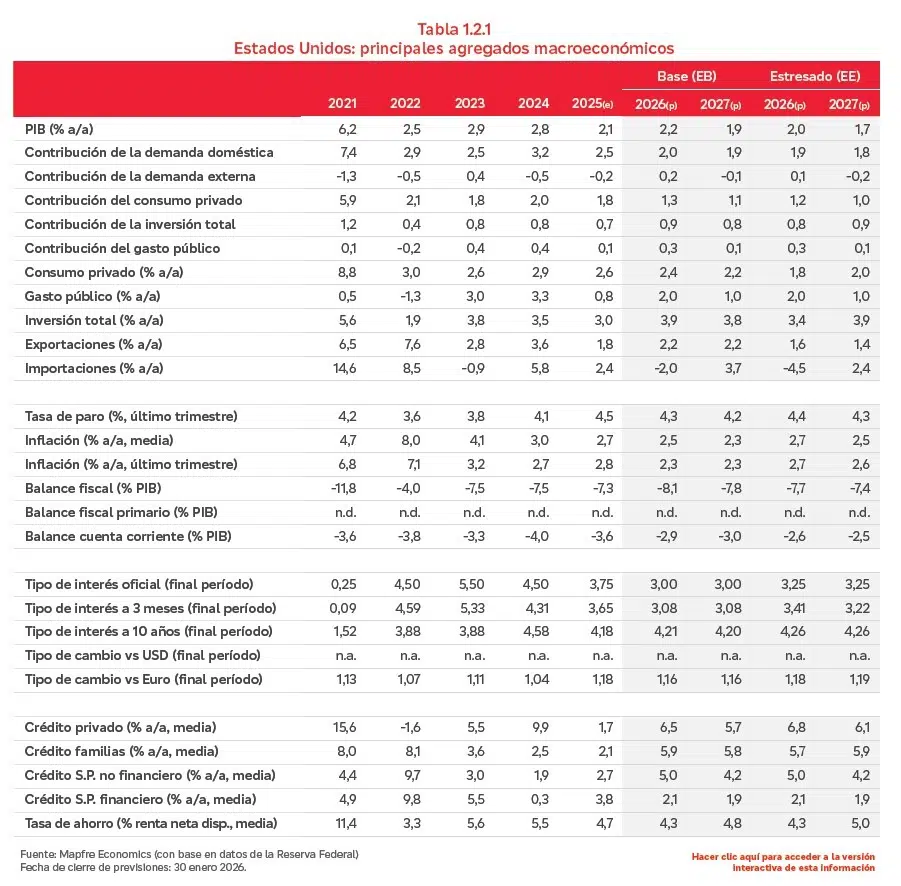

The US economy is projected to grow 2.2% this year and 1.9% next, with inflation expected at 2.5% and 2.3%, respectively, according to Mapfre Economics’ 2026 Economic and Industry Outlook. The report identifies geopolitics as a key driver that’s reshaping the economic cycle and redefining the response of monetary and fiscal policies.

“The persistence of geopolitical tensions, more than their intensity, is the main short‑term risk in the economic outlook,” Mapfre Economic Research noted in February, a point that has taken on renewed significance this week amid joint US and Israeli strikes on Iran and Tehran’s subsequent retaliation. Ayatollah Ali Khamenei, Iran’s Supreme Leader since 1979, died as a result of the operations.

Eduardo García Castro, an expert economist at Mapfre Economics, points out that there are three factors that will determine the macro-financial dynamics of this conflict: the duration and intensity of hostilities, the integrity of critical infrastructure, and the management of the Strait of Hormuz, through which around one-fifth of the world’s oil and a substantial portion of its liquefied natural gas (LNG) transits.

Mapfre Economics notes that, beyond geopolitical concerns, one of the main short-term risks to the US economy is the deterioration of the fiscal trajectory and its potential impact on borrowing costs. The federal deficit was approximately 6.2% of GDP at the end of 2024 and is expected to remain high in the coming years: official estimates project the deficit to be around 6.2% of GDP in 2025 and about 5.8% in 2026, outlining a fiscal trajectory that’s clearly unsustainable over the medium term.

This situation has been flagged as a concern by the Federal Reserve, the Congressional Budget Office, the International Monetary Fund (IMF), and the major credit rating agencies. Amid high interest rates and the Federal Reserve’s shrinking balance sheet, the persistent rise in financing needs underlies the recent spikes in Treasury yields and the ongoing debate over structural demand for US bonds, particularly from foreign investors.

The fiscal package approved in July, known as the “One Big Beautiful Bill,” exacerbates these risks. It includes tax deductions for overtime, tips, and Social Security contributions, as well as substantial increases in defense and immigration spending. Meanwhile, it removes incentives for electric vehicle purchases and gradually phases out other tax credits linked to the Inflation Reduction Act (IRA), while also anticipating cuts to Medicaid.

The Congressional Budget Office estimates that the package could add between $2.4 trillion and $3 trillion to the deficit and debt over the next decade, while the government maintains that higher growth will generate offsetting revenues—a hypothesis widely questioned by analysts.

Suspension of tariff agreements

The Supreme Court ruled that the tariffs imposed by the executive branch were illegal, a decision that marks a turning point in US trade policy.

“The Supreme Court’s decision not only brings an exceptional period to a close—one in which the White House extended tariffs to virtually all of its trading partners—but also requires a reassessment of the legal framework that will underpin tariff strategy in the months ahead. The implications extend beyond the legal dimension, encompassing the broader climate of regulatory uncertainty, the reconfiguration of corporate and investor incentives, and the potential redirection of trade flows going forward,” emphasizes García Castro in a recent report.

Moreover, Mapfre Economics noted in its February report that the combination of persistent fiscal imbalances, tighter financial conditions, and escalating geopolitical tensions poses a significant risk to the US economy and the stability of the global economic system, given the United States’ heavy reliance on external savings to finance its deficit.