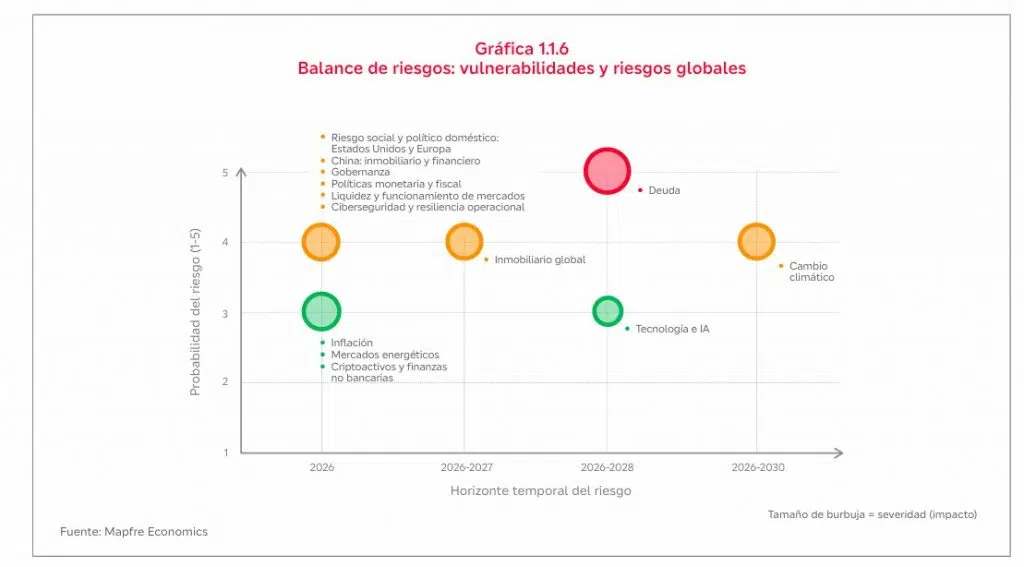

Mapfre Economics, Mapfre’s research arm, has developed a risk map for its report Economic and Industry Outlook 2026, highlighting the factors that could affect the performance of the global economy and in which debt has taken on growing importance.

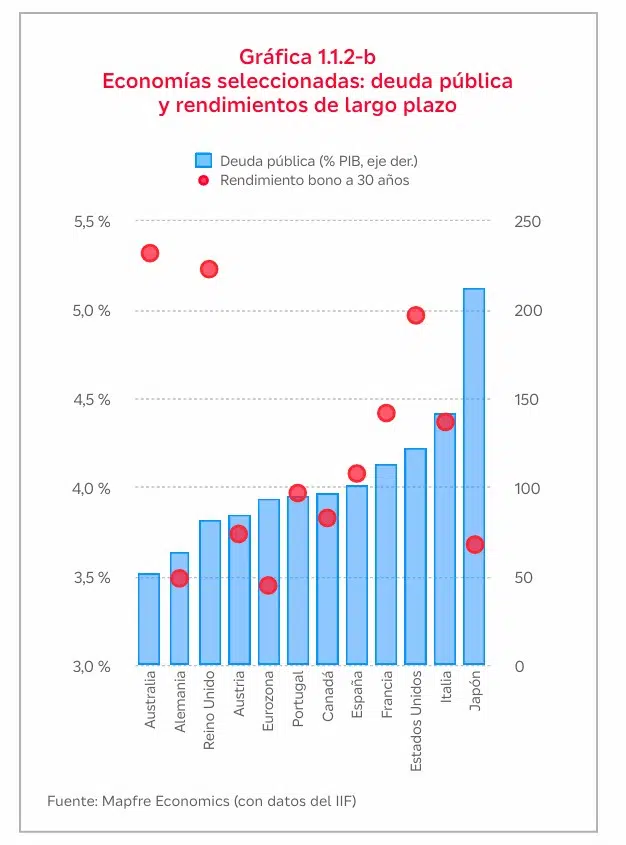

The United States is one of the countries causing the greatest concern among economists and national and international institutions, which identify the deterioration of its fiscal path and its potential impact on financing costs as risks to its economy. The federal deficit closed 2024 at around 6.2 % of GDP and is expected to remain elevated in the coming years. Official estimates place the deficit close to 6.2 % of GDP in 2025 and around 5.8 % in 2026, outlining a fiscal path that is clearly unsustainable in the medium term.

The persistent increase in financing needs, in a context of high interest rates and the Federal Reserve’s (Fed) balance sheet reduction, lies behind the recent rise in U.S. Treasury yields and the growing debate about structural demand for U.S. bonds, particularly among foreign investors.

The deficit has widened further with the “One Big Beautiful Bill,” which extends tax cuts and increases spending in priority areas, providing stimulus while postponing fiscal adjustments. “The U.S. Treasury has emphasized financing through bond issuance and hinted that it is considering future coupon increases; the market is already pricing in a steeper yield curve as a sign of concern about fiscal excesses and a more volatile term premium,” Mapfre Economics notes in its report.

It also explains that a “debt scare” could trigger more aggressive auctions, pressure in the 10- to 30-year segments, and Treasury buybacks with a bias toward implicit yield-curve control. “Fiscal discipline appears to be a prerequisite for anchoring expectations,” the report adds.

However, the debt problem is not exclusive to the United States. In Europe, the shift toward higher spending on defense and infrastructure, combined with the revision of fiscal rules, could exacerbate political and economic tensions within governing coalitions. Electoral processes and the renegotiation of fiscal packages in 2026 will be critical points that could affect the region’s stability.

Other risks threatening the global economy

Governance risks at the global level remain high due to the persistence of protectionist measures, the use of tariffs as a negotiating tool, and the possibility of coordinated retaliatory measures. The European Union, Canada, and Mexico have already been subject to announcements of broad or sector-specific tariffs by the United States government, along with threats of further increases if deficits are not rebalanced or specific concessions are not granted. This undermines regulatory predictability and legal certainty in global value chains, raises cross-border costs, and may erode investment, particularly in complex manufacturing sectors such as automotive, machinery, and aerospace.

Regarding monetary policy, Mapfre Economics notes that convergence toward “neutral” interest rates is not guaranteed and also warns of inflation risks.

China, for its part, faces risks related to its real estate debt and financial debt. The high level of indebtedness among companies and local governments is adding pressure to its banking system, increasing the risk of liquidity crises. At the same time, emerging economies such as Brazil and Turkey face similar challenges, with high levels of external debt that make them vulnerable to fluctuations in international markets and to monetary policy decisions in developed countries.