Inflation, which has reached historical highs, refers to the cost of living and is a barometer that determines actions with strong implications for the economy, which are becoming even more aggravated against the backdrop of the geopolitical crisis. So, these types of statements ring true. And the ultimate consequence of rising prices is that consumers pay more, which can erode business’ results. But, as seen in the latest meetings of the central banks, this situation also alters monetary policy, which plays an essential role in keeping recovery on track and allowing the most indebted countries to continue paying low interest rates on the money they borrow in the markets.

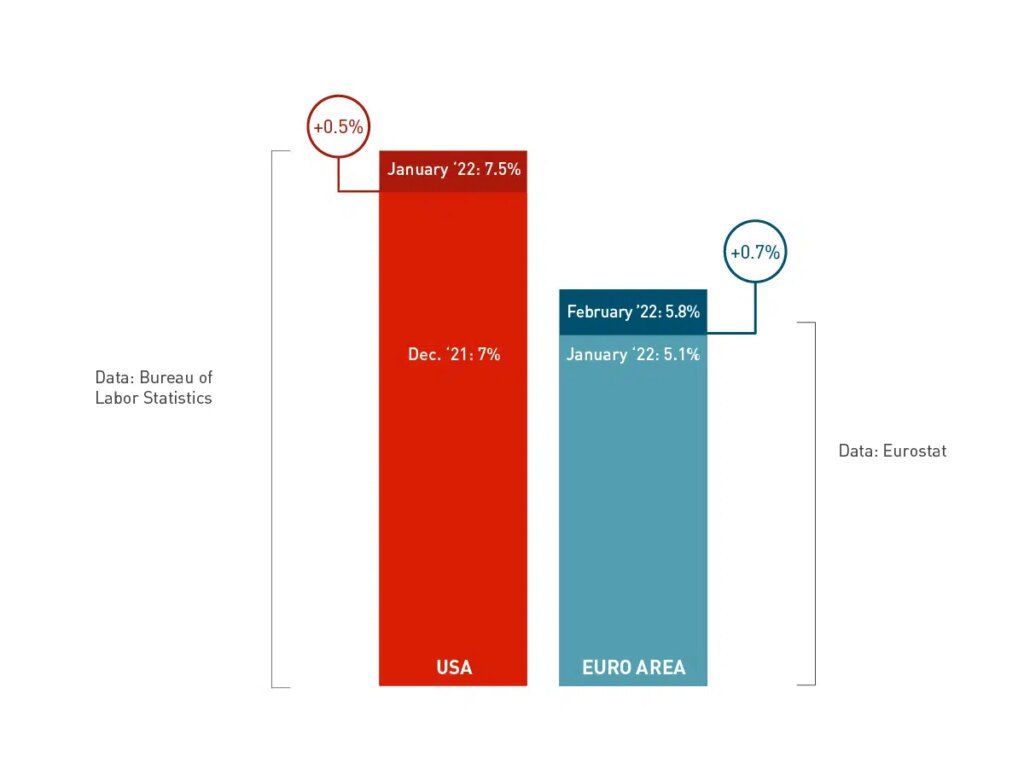

At this time, prices are soaring on both sides of the Atlantic, and due to the war in Ukraine, the upward trend will surely continue. According to the latest data from Eurostat, year-on-year inflation in the Eurozone was 5.8% in February, seven-tenths above the increase observed in January, which represents the steepest price increase in the euro region in the entire historical series. In the United States, the Bureau of Labor Statistics reported that inflation rose to 7.5% in January, half a point above its level in December, the highest since 1982. And in Spain, it also stood at 7.4% in February, its highest rate in 33 years.

Until now, despite shattering long statistical records, this data had not set off all the alarm bells. This was because some of the factors causing these spikes were purely short-term (besides the fact that what statisticians call the ‘base effect’ was taking place), convincing many experts that these levels could be temporary. But this outlook has radically changed, and that camp has been all but abandoned as a consequence of the war.

People are even starting to talk about the possibility of stagflation, that is, a scenario of greater price pressure and economic stagnation or even recession. “The short-term rebound in commodities, coupled with new displacements in global transport as a result of geopolitical dynamics, would prolong the persistent effects on global inflation, altering the outlook for a peak in inflation throughout 2022 and postponing the forecast of inflation rates staying within the central banks’ band in the medium term,” adds Gonzalo de Cadenas-Santiago, executive director of Mapfre Economics. Funcas, with Mapfre Economics participating on its panel, calculated last week that prices in Spain could skyrocket by 6.5% on average this year, almost two points above its pre-conflict forecast, but events are developing so quickly that this estimate may have fallen short. If these forecasts are confirmed, household purchasing power would be severely impacted, causing the recovery of private consumption to stagnate with a very significant impact on growth.

This inflation, which originally arose from a transitory shock in energy and transport costs, persistently changes relative prices and puts pressure on nominal revisions, such as salaries or pre-established prices (for example, rents). This would trigger what are known in economic circles as “second-round effects,” starting that unwelcome vicious circle of inflation. “These and other factors suggest that we will face structurally higher inflation after the current upturn,” explains De Cadenas-Santiago. However, in this current environment of conflict, the expert believes that measures will be taken from the regulatory standpoint to make this happen.

Mapfre Economic Research adds that, even prior to war breaking out, energy prices seemed likely to climb persistently over time, whether through the green transition and the internalization of production externalities, or the search (always deficient at the outset) for new energy sources, which will be expensive, at least in the short term. “This is especially worrisome in Europe, which is heavily dependent on both energy and raw materials that make possible a green alternative (lithium, rhodium, rare earths, etc), given that it is hemmed in by geopolitics at all its cardinal points. At the same time, the region is held captive by commitments that are sometimes hard to justify (such as nuclear power in Germany).” This is again compounded by the problems arising from supply chains, which are being aggravated by the semiconductor crisis and the high dependence on China.

But why are energy prices so decisive in determining the evolution of inflation? To calculate the CPI, a selection of products and services is made that resembles an average household’s consumption. Electricity has a weight of almost 3% in the CPI basket, and yet it has skyrocketed to the point that in 2021 it was responsible for nearly half of all inflation. In addition, the new highs reached by gas and oil due to the geopolitical conflict have not yet been transferred. In short, these prices, which have been extremely volatile in recent months, can determine key decisions that end up affecting citizens as follows. Below is a list of the consequences of the rising cost of living:

- Salaries: As indicated above, higher inflation can lead to higher salaries and, as a consequence, cause the feared second-round effects. This can happen in two ways. In some cases, a direct increase through CPI-linked salary review clauses. In others, through upward collective bargaining, when the wage increases in the following year’s agreement are negotiated. However, this effect is likely to be contained in the face of the new economic uncertainty generated by the conflict.

- Pensions: in some countries, like Spain, the annual increase is indexed to the CPI, so the price calculation determines how much benefits are revalued annually. This measure, which is seemingly good news for the pensioner, means that, in turn, the item of expenditure in the budgets for pensions increases, allowing less money to be allocated to other resources.

- Rent: The CPI is also used as a reference in many rental contracts. Depending on how this clause is included, inflation has a significant impact on the cost of housing for tenants. That being said, against a backdrop of international crisis like the current one, governments could limit this phenomenon.

- Interest rates: Central banks have price control as one of their main mandates. In the case of the European Central Bank, in fact, it is the main one: “Our job is to maintain price stability. This is the best contribution monetary policy can make to economic growth and job creation,” the ECB explains. Specifically, its target is an inflation rate of 2% in the medium term. It can use different tools to achieve this, such as raising interest rates, which directly increases the price of money. “Higher inflation, in theory, would lead to a more aggressive ECB. But that isn’t the case here. Inflation exclusively due to energy cannot be combated with higher interest rates (this was clarified by ECB Chief Economist Phillip Lane, a few days ago),” explains Alberto Matellán, chief economist at Mapfre Inversión. This has significant consequences for the most indebted countries, for example. It also comes at a time when this debt has grown considerably as a result of the pandemic. Furthermore, it puts pressure on the monetary institutions to gradually withdraw the monetary stimuli introduced during the latest crises, with consequences for the financial markets. Again, economic uncertainty could cause the monetary institutions to put on the brakes.

- Shopping basket: In Spain, the latest complete CPI data, published by the National Statistics Institute, shows that food and beverages were 5% more expensive in December of last year than in the same month of 2020. Prices of food and non-alcoholic beverages have not risen so significantly since September 2008.

- Savings: another major risk, due to the above, is the loss of purchasing power that inflation causes in household savings. Inflation causes money to lose value and erodes our purchasing power.